My bad credit score made apartment hunting in Toronto a nightmare

By: Dominic Licorish on March 7, 2017

I turned 25 in January. Up until now, I’ve been living with my parents, sheltered from the realities of Toronto’s pricey housing market. But hitting 25 made me realize, “Oh, shit, I’m actually an adult.”

And adults aren’t supposed to live with their parents, right?

It was time to get my own place. I was tired of commuting halfway across the city from Scarborough to get to work and cutting my nights out short in order to trek back home.

Toronto is one of the most expensive rental markets in the country. My salary is just shy of $40,000 a year, before taxes. The average rent for a bachelor in the city is currently going for $1,517 per month (according to the Toronto Real Estate Board), which would pressure my monthly budget.

I quickly noticed that the majority of landlords also wanted a credit report with applications

I knew I had to find a roommate and save money by splitting a two bedroom. Those have an average rent of $2,567. Fortunately, I had a friend with a similar income level also looking for a place. When we started looking at apartments, I quickly noticed that the majority of landlords also wanted a credit report with applications.

That’s where my hunt went downhill.

If you’re looking for a happy ending, you won’t find one. This is a story about rental heartbreak. But I did learn a few things in my failed attempt to fly from the nest.

Everything is more complicated

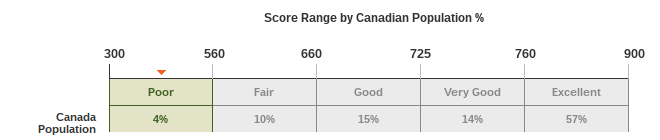

Finding a good apartment in Toronto is a colossal task and prices are really just the beginning. The worst part is just how competitive it is. Having a low credit score makes you that much less desirable than other applicants. And my credit score is downright bad. According to Equifax, at 555, my score is worse than 96% of Canadians. It meant that no matter how secure my job is, it was hard to convince landlords that I could be relied upon to consistently make rent on-time.

There was one apartment we were in the running for that we both loved. It was a newly renovated basement apartment with its own entrances, new appliances and hardwood floors — all in an awesome neighbourhood with great transit access. The landlord picked us as the front runners. He liked us as people. He liked our jobs (my friend works for an investment firm). He told us the apartment was ours — all we needed to do was send him our Equifax reports. My heart dropped, knowing how bad mine would look.

He was looking for a minimum credit score of 560, which falls into the “fair” bracket on Equifax’s scale. Mine at 555, was “poor”.

My score is the legacy of poor choices during college, when I left credit card balances unpaid.

The landlord was somewhat sympathetic. He said he could tell I was serious about fixing my finances. He gave us a few options for how we could secure the place even with my low credit score, but it ended up complicating things, because we had to scramble to meet these more stringent demands.

Have money saved before going on the hunt

Part of the difficulty of the apartment hunt was that neither of us had our deposits saved up. In fact, I wouldn’t have had enough money to afford the first and last month deposit until just a few days before the beginning of March, which was cutting it way too close. My friend, however, wanted to move ASAP.

He was looking for a minimum credit score of 560, which falls into the “fair” bracket on Equifax’s scale. Mine [was] at 555

When the landlord saw that I had a low credit score, he gave us the options of finding someone to cosign the lease with us, leaving my name off the lease as a tenant so that only my friend (whose score was more acceptable) would be held accountable to the landlord, or paying an extra two months up front with our deposit.

We decided not to get our parents involved and pay the extra money up front. I was fully prepared to live off of nothing but ramen and even take out a payday loan if need be, even though I know just how terrible that cycle is. I wanted the apartment badly, so I was willing to do whatever I needed.

Even a guarantor isn’t a guarantee

In the end, even though the landlord was cool with the increased deposit, he ended up insisting on a guarantor at the last minute. We’d just sent the first half of the deposit through e-transfer and suddenly he was changing terms.

Still, in just a couple of hours, I was able to get my mom, who lives in Calgary, to sign the required form and attach her credit report to prove that she could be relied on to pay rent if we didn’t. Why my mom you ask? Well, because my roommate’s parents said no to cosigning, and my dad also refuses to cosign for anyone on principle.

About three days after we got the apartment, we lost it. I felt like a bum, because if my credit score had been higher, none of this would have happened

After jumping through all these hoops, the landlord told us he decided to move forward with different tenants. He said there was too much back and forth and he just wanted it over with.

That was it. About three days after we got the apartment, we lost it. I felt like a bum, because if my credit score had been higher, none of this would have happened.

People don’t look at you as a responsible adult

I could see a shift in the way the landlord and even my roommate treated me when my bad credit score was revealed. Suddenly, I wasn’t an equal partner in the negotiations. I was relegated to the backseat.

It’s not a great feeling, knowing that people don’t respect you as much because of one stupid little number, but it also taught me a lot about just how important that number is. Having good credit is a sign of maturity and responsibility, and clearly, I haven’t been as mature or responsible as I should have been with my money.

Don’t give up

Losing the apartment sucked. When we got that call, there was only seven days left in the month. Finding another place would be stressful. I decided I’d give up on moving out—for now.

What I haven’t given up on is fixing my score and building up my savings to comfortably handle the competitiveness of the Toronto rental market. I’m still going to try and move out before I turn 26. That gives me a year to get it right.

By then, I intend my credit score to be an asset, instead of a liability.